If you trade stock derivatives, you need to know about physical settlement. This is a process where you have to deliver or receive the underlying shares when your contracts expire. SEBI has implemented physical settlement for all equity derivative contracts to reduce speculation and manipulation. In this blog, we will explain how physical settlement works and what are the policies and procedures that FYERS follows.

Physical settlement applies to all stock futures and options contracts that are open on the expiry day. These contracts are settled by delivering or receiving the underlying shares instead of cash. The number of shares to be delivered or received is determined by multiplying the lot size by the number of contracts.

The contracts that are subject to physical settlement are:

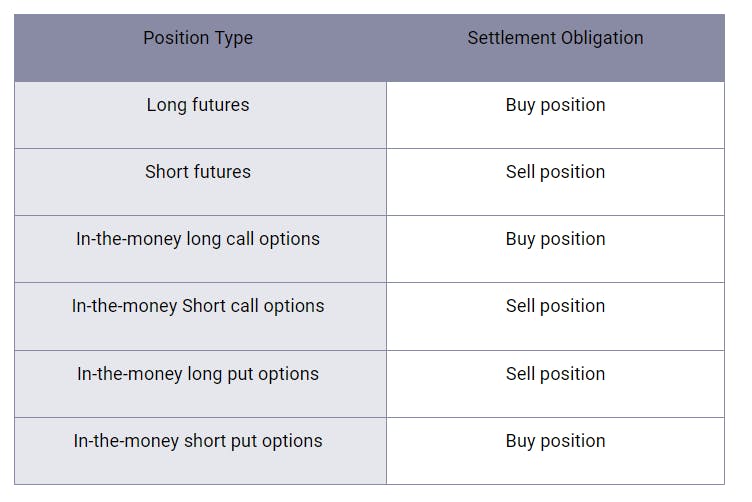

Long or short futures positions that are open after the closing session on expiry day.

In-the-money (ITM) options positions that are exercised and assigned. ITM options are those where the strike price is favorable compared to the market price of the underlying stock. For example, a call option with a strike price of 100 is ITM when the stock price is 110, and a put option with a strike price of 100 is ITM when the stock price is 90.

The value of the shares to be delivered or received is calculated based on the final settlement price of the contract for futures and the strike price for ITM options.

Physical settlement of shares is done through CDSL/NSDL depositories on Expiry + 1 day, as per the schedule set by the Clearing Corporation. However, in some cases, positions may be 'net off' to avoid physical delivery. This process involves offsetting positions in stock derivatives contracts, such as futures and options, to reduce the need for actual delivery of shares. For example, if you have both a long position in a futures contract and a corresponding options position (e.g., a long futures and a put option), these positions may be netted off against each other before the expiry, resulting in no need for physical settlement. You can refer to Annexure 1 of NSE circular 67/2018 dated 15th June 2018 for more details on the process.

Depending on your position type, you will have different settlement obligations:

Delivery margins are extra funds that you need to maintain in your account if you have positions in stock derivatives that are likely to result in delivery of the underlying shares. These positions include futures contracts and In-the-money (ITM) long call options. Delivery margins are charged by the exchange to ensure that you can afford to take or give delivery of the shares when the contract expires.

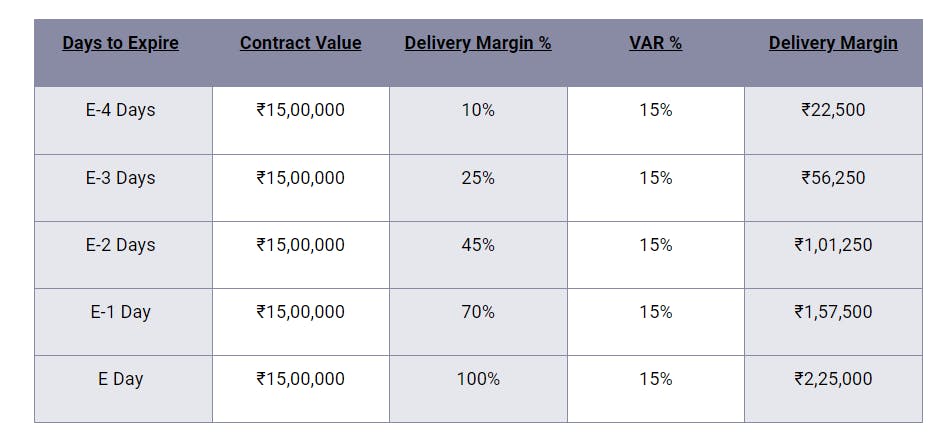

Delivery margins are calculated as follows:

Delivery margin = Strike price x Quantity x Delivery margin % x VAR %

*VAR = Value At Risk

For example, suppose you have bought 1 lot (500 Qty) of Reliance 3000 CE contract that expire on March 22. This means you have the right to buy 500 shares of Reliance at ₹3000 each on March 22. If the current market price of Reliance is ₹3100, your option is ITM and you will have to pay delivery margin. Let’s say the delivery margin percentage is 10% and the VAR percentage is 15%. Then your delivery margin on E-4 Day (Friday EOD) will be:

Delivery margin = 3000 x 500 x 10% x 15% = ₹22,500

E-4 means Expiry Day minus 4 days - 4 days before expiry

The delivery margin percentage and VAR percentage are set by the exchange and may change depending on the volatility and liquidity of the underlying stock. The delivery margin also increases as the expiry date approaches. Here is a table that shows the delivery margin required for different days before expiry:

Please note that this is the delivery margin required for one lot as per the exchange. If you have multiple lots, you will have to maintain a delivery margin for each lot as per the calculation above.

Starting from E-4 BOD (Beginning Of Day), delivery margins will be applied to both existing and new positions. This is only applicable to trades done under 'Margin/Invest' product type. (Not applicable for Intraday/CO/BO product type)

Further, starting with the March 23 expiry, there will be net settlement of the cash and futures segments upon expiry of stock derivative contracts. This means that you will not have to take or give physical delivery of the shares, but only pay or receive the difference between the contract price and the settlement price.

The DNE (Do Not Exercise) facility has been discontinued by the exchange. This means that you cannot opt out of exercising your ITM options before expiry.

As a trader, you need to be aware of FYERS policies regarding physical settlement and follow them accordingly. Here are some important policies that you should know:

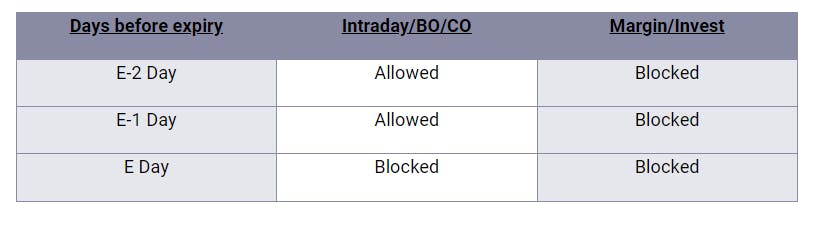

One of the policies you need to know is blocking contracts in current month expiry contracts. This means that you cannot trade in near-month contracts using certain product types during the expiry week. The table below shows the product types and the days when they are blocked or allowed:

If any product type for the current month’s contract is blocked, you can trade in the next month's contract.

To carry forward your positions, you need to maintain a percentage of the contract value as margin. The percentage depends on the position type and the contract expiry.

The contract value is calculated by multiplying the lot size by the final settlement price for futures and the strike price for options.

If you do not maintain sufficient margins, FYERS will square off all your open positions in near-month contracts. Additionally, to streamline the settlement process and avoid unnecessary physical delivery, FYERS may also 'net off' certain positions. This means that if you hold both a long and short position in related contracts (like a future and an option), these can be netted off to eliminate the need for physical delivery, minimizing the impact on your account balance.

You are responsible for any trade losses incurred during position closure.

To avoid automatic square off of your positions, you must have sufficient margins in your account. The required fund limit is equal to or greater than the contract value of your derivative positions.

If you fail to maintain sufficient balances, FYERS may close your positions, and any resulting losses will be borne by you.

The delivery margin percentage could be higher than the exchange percentage to avoid any risks or complications.

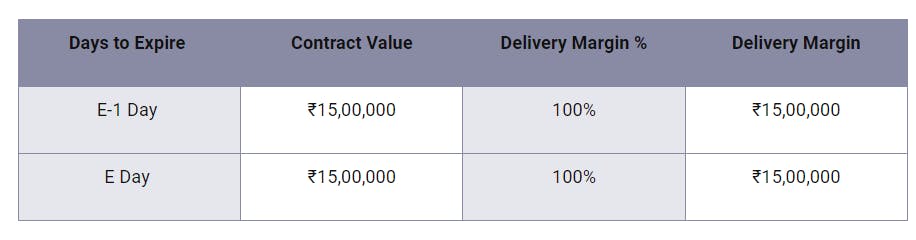

For E-4, E-3, and E-2 days, FYERS charges the same delivery margin percentage as the exchange. You can refer to the table in the previous section for the exchange delivery margin percentage. However, the delivery margin percentage is 100% of the contract value on E-1 and E day as shown in the table below:

If you want to take delivery of a futures contract, you need to inform FYERS via email and ensure that you have sufficient fund limits at the time of intimation. If you fail to do so, your position may be squared off by FYERS.

You need to have a FYERS Demat account to opt for physical delivery.

Short delivery of shares will attract a 20% penalty based on the value of the shorted stock.

FYERS will charge a brokerage fee of 0.2% on the physical settlement value to compensate for processing efforts and risks.

Debit balances will incur a daily interest charge of 0.05%.

We hope this blog has helped you understand the concept of physical settlement and how it affects your trading. If you have any queries or feedback, please feel free to comment below or contact us at support@fyers.in.

Happy Trading!